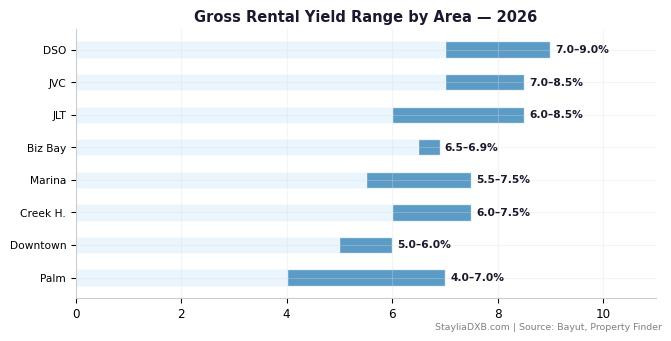

Here's something that's been bugging me about the Dubai investment conversation: everyone talks about Marina, Downtown, and Business Bay, but almost nobody talks about JLT — even though it's literally across the road from Marina and delivers better yields at a 25–30% discount.

JLT (Jumeirah Lake Towers) is the classic "unsexy but profitable" play. No flashy waterfront, no Burj view, no celebrity chef restaurants. Just solid fundamentals, strong rental demand, and price-per-square-foot numbers that actually make the yield math work. It's the kind of area that doesn't get Instagram posts but gets bank deposits.

I went through DLD transaction data, Bayut and Property Finder listings, cluster-by-cluster performance metrics, and service charge filings. Here's everything you need to know — investor to investor.

Pricing: AED 1,960/sqft Average — Marina Living at JVC Pricing

JLT's average price per square foot sits at approximately AED 1,960 as of early 2026, according to DXB Interact and Property Finder data. That puts it in a sweet spot: 25–30% cheaper than neighboring Dubai Marina (AED 2,661/sqft) but 45% more expensive than JVC (AED 1,150/sqft). You're getting a mature, well-connected community at mid-market pricing.

Transaction prices by unit type: Studios: AED 500,000–750,000. 1-bedrooms: AED 750,000–1.2 million. 2-bedrooms: AED 1.2–1.8 million. 3-bedrooms: AED 1.6–2.5 million. Office spaces: AED 600,000–1.5 million (JLT has a significant commercial component).

DLD data shows approximately 5,500 residential transactions in JLT in 2024. The split is heavily resale-dominant — roughly 80% secondary market — because JLT is a mature community with virtually no new supply. This resale dominance is actually a major positive for investors: prices reflect real market dynamics, not developer marketing.

Capital appreciation: prices are up roughly 45–55% from 2020 lows. The appreciation rate has been tracking slightly behind Marina (which benefited more from the luxury surge), but JLT's more affordable price point means the percentage returns on invested capital are competitive. And looking ahead, JLT is projected to see 8–10% price growth in 2026 as the value gap with Marina becomes increasingly apparent to buyers.

The JLT Layout: Understanding Clusters

Source: DLD transaction records & Property Monitor. StayliaDXB analysis.

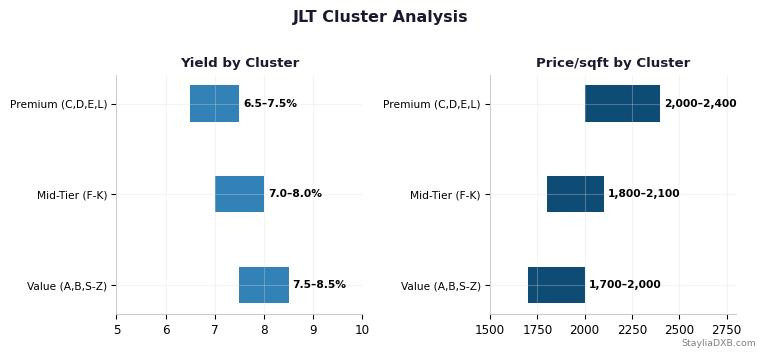

If you're not familiar with JLT's layout, it's essential to understand before investing. JLT is organized into 26 clusters (A through Z), each cluster containing 3–4 towers arranged around shared facilities. Some clusters have direct lake views, some face Sheikh Zayed Road, and some are interior-facing. The cluster location dramatically affects pricing, rental demand, and resale liquidity.

Premium clusters (lake-facing): Clusters C, D, E, L, N, O, and T. These overlook the artificial lakes and have walkable access to the JLT promenade with restaurants, cafes, and retail. Units here command a 10–15% premium over interior clusters. If you're buying for appreciation, buy lake-facing.

Mid-tier clusters: Clusters F, G, H, I, J, K, P, Q, R. These are set back from the lakes but still have good access to retail and metro stations. Solid rental demand at more reasonable prices. If you're buying for yield, this is where the numbers work best.

Value clusters: Clusters A, B, S, U, V, W, X, Y, Z. Further from the lakes, less retail nearby, and sometimes noisier due to Sheikh Zayed Road proximity. Lowest prices but also lower tenant demand. I'd generally avoid these unless you're getting a significant discount — the rental void periods can eat into your yield advantage.

Rental Yields: 6–8.5% Gross — Consistently Strong

Source: DXB Interact & Property Monitor rental data. StayliaDXB analysis.

JLT's rental yields are among the best for a mature, well-connected community in Dubai. Here's the breakdown:

Studios: Average rent AED 45,000–60,000/year. Purchase price AED 500K–750K. Gross yield: 7.5–8.5%. Studios in JLT are perennially in demand from young professionals, especially those working in JLT's DMCC free zone offices. Vacancy rarely exceeds 2 weeks between tenants.

1-Bedrooms: Average rent AED 65,000–90,000/year. Purchase price AED 750K–1.2M. Gross yield: 7–8%. The bread-and-butter of JLT investing. Furnished 1-beds near Cluster D or E (close to Almas Tower and DMCC metro) perform best.

2-Bedrooms: Average rent AED 90,000–130,000/year. Purchase price AED 1.2–1.8M. Gross yield: 6.5–7.5%. Family demand is solid — JLT's schools, parks, and proximity to Marina means families who can't afford Marina often settle in JLT.

3-Bedrooms: Average rent AED 130,000–170,000/year. Purchase price AED 1.6–2.5M. Gross yield: 6–7%. Less liquid but strong for family tenants who need space.

Service charges in JLT are generally reasonable at AED 12–18/sqft — lower than Marina (AED 15–25/sqft) and significantly lower than Downtown or Palm. On a 850 sqft 1-bed apartment, that's AED 10,200–15,300/year. Net yields after service charges typically run 5.5–7% — beating most comparable areas in Dubai.

Tower-by-Tower: Where the Smart Money Parks Itself

Goldcrest Views (1 & 2) — Cluster J: AED 1,800–2,200/sqft. Well-maintained towers with good layouts. About 75 transactions in 2024. Consistent tenant demand. Yields: 7–7.5% gross. One of my go-to recommendations for first-time JLT investors.

Lake Shore Tower — Cluster Y: AED 1,700–2,000/sqft. One of the few towers with genuine lake frontage in a value cluster. Service charges are reasonable at AED 13/sqft. Yields: 7.5–8% gross. The catch: Cluster Y is on the periphery, so tenant pool is slightly smaller.

Saba Towers (1, 2 & 3) — Cluster E: AED 2,000–2,400/sqft. Premium cluster with lake views and proximity to DMCC metro station. Strong tenant demand from DMCC professionals. Yields: 6.5–7.5% gross. Lower yields than periphery towers but better appreciation and liquidity.

Icon Tower (1 & 2) — Cluster L: AED 2,100–2,500/sqft. Lake-facing premium towers. Modern finishes, good amenities. About 60 transactions in 2024. Yields: 6.5–7% gross. If you want the "best address" in JLT, this is it.

Concorde Tower — Cluster D: AED 1,900–2,200/sqft. Great location near the promenade. Older build but well-maintained. Yields: 7–7.5% gross. Reliable performer.

Global Lake View — Cluster C: AED 1,800–2,100/sqft. Mixed-use tower with offices and residential. Direct promenade access. Good for short-term rentals due to the walkable restaurant scene. Yields: 7–8% gross.

Bonnington Tower — Cluster J: AED 2,200–2,600/sqft. Premium hotel-residence with Bonnington brand management. Higher service charges (AED 20–22/sqft) but consistent occupancy through the hotel pool. Yields: 6–6.5% gross on long-term, potentially 8–9% on short-term through the hotel operator.

Towers to be cautious about: Some older towers in clusters A, B, V, and W have higher-than-average service charges relative to their rental income, persistent maintenance issues, or weak tenant demand. Always check the service charge history and RERA rental index for the specific tower before buying.

The DMCC Advantage: 22,000+ Companies and Counting

JLT's biggest structural advantage — the one most casual investors overlook — is the DMCC (Dubai Multi Commodities Centre) free zone. DMCC is the world's largest free zone by number of member companies, with over 22,000 registered businesses as of 2025.

Those 22,000+ companies employ tens of thousands of professionals, many of whom prefer to live within walking distance of their offices. This creates a captive tenant pool that is remarkably stable and predictable. When the economy softens, DMCC companies still need staff, and those staff still need housing.

The DMCC effect shows up in the data: JLT's vacancy rates run 3–5% — among the lowest in Dubai for a non-luxury community. That's comparable to Downtown and Marina, despite JLT's lower price point. Low vacancy plus high yields equals strong risk-adjusted returns.

Metro Connectivity: DMCC Station and Beyond

JLT is served by the DMCC metro station on the Red Line — one of the most heavily trafficked stations in Dubai. This gives residents direct metro access to Marina, Internet City, Media City, Barsha, Mall of the Emirates, DIFC, and Downtown. The 20-minute metro ride to DIFC is a key selling point for finance professionals who don't want to pay Downtown prices.

This metro connectivity is a permanent infrastructure advantage. Unlike speculative catalysts (like Creek Tower or the Blue Line), the Red Line is already operational and heavily used. It's baked into JLT's value — and it's one reason why JLT's rental demand is so resilient.

Supply Pipeline: Virtually Zero New Stock

Like Dubai Marina, JLT is essentially built out. There are no significant new residential projects in the pipeline. The community's 87 towers are the towers — no more are coming. This supply constraint is JLT's second-biggest structural advantage (after DMCC).

When you buy in JLT, your competition is other resale units, not developer inventory with 5-year payment plans. This means less downward pressure on prices during market corrections and more stable rental rates. During the 2019–2020 downturn, JLT prices dropped less than JVC, International City, or even parts of Business Bay — largely because there was no new supply to absorb.

Short-Term Rentals: The JLT Sweet Spot

JLT has emerged as a strong short-term rental market, benefiting from its proximity to Marina (tourists want the Marina lifestyle but JLT units are 25–30% cheaper to operate), the walkable promenade with restaurants and cafes, and the metro connectivity to tourist attractions.

AirDNA data shows average occupancy of 72–78%, average daily rates of AED 350–550/night for a furnished 1-bed, and annualized gross income of AED 120,000–160,000. Compared to long-term lease income of AED 70,000–90,000, that's a 45–75% premium.

Net short-term rental yield after management fees, furnishing amortization, DTCM licensing, and utilities: approximately 7–9%. That makes JLT one of the best risk-adjusted short-term rental plays in Dubai — you get 80% of Marina's tourist appeal at 70% of the cost.

JLT vs Dubai Marina: The Honest Comparison

Since they're neighbors, the comparison is inevitable. Here's how they stack up:

Price/sqft: JLT AED 1,960 vs Marina AED 2,661. Advantage: JLT (25% cheaper).

Gross yield: JLT 6–8.5% vs Marina 5.5–7.5%. Advantage: JLT (0.5–1% higher).

Capital appreciation potential: Marina has the brand premium and waterfront, but JLT's value gap is closing. Slight advantage: Marina, but JLT may outperform on a percentage basis.

Tenant demand: Both excellent. Marina has tourism pull; JLT has DMCC employment pull. Tie.

Liquidity: Marina is more liquid for resale. Advantage: Marina.

Service charges: JLT AED 12–18/sqft vs Marina AED 15–25/sqft. Advantage: JLT.

Supply risk: Both essentially built out. Tie.

The verdict: if you have the budget for Marina and prioritize brand/lifestyle, Marina wins. If you're optimizing for yield and net returns, JLT is objectively the better math. For most investors, having one in each makes sense as a diversification play.

Who Should Buy in JLT?

Yes, buy if: You want Marina-adjacent living at a 25–30% discount. You're yield-focused and targeting 7%+ gross returns. You value metro connectivity and the DMCC tenant pool. You want constrained supply and stable rental demand. You're looking for short-term rental potential without Marina's premium pricing. Your budget is AED 500K–1.5M and you want the best possible returns in that range.

Think twice if: You need the prestige of a waterfront address — JLT doesn't have it. You're buying a 3-bed hoping for strong rental demand — family units are less liquid in JLT. You're looking at a tower in a peripheral cluster without researching the specific tenant demand. You're expecting Downtown-level capital appreciation — JLT's growth is steadier but less dramatic.

The Bottom Line

JLT is the most underappreciated investment area in Dubai's core. It delivers yields that rival JVC and DSO, but with the infrastructure, connectivity, and tenant stability of a mature community. The DMCC free zone provides a captive tenant pool that most other areas can't match. And with zero new supply coming, your rental income is protected against the dilution risk that haunts Business Bay, JVC, and other supply-heavy areas.

The smart play: studios or 1-beds in Clusters D, E, J, or L, priced at AED 1,800–2,200/sqft, with service charges under AED 16/sqft. Furnish them, target DMCC professionals or short-term tourists, and let the yield compound.

If you want to compare specific JLT towers, get my current picks for the best cluster/floor combinations, or just talk through whether JLT fits your strategy — reach out.