I'm not an agent. I don't get a commission if you buy a distressed unit in JVC or a fresh one in Business Bay. What I do have is 35 years of my family's money in commodity trading and raw land, and, more recently, over $40 million in real estate equity — most of it built the same way every time: buy right, not often.

So I ran an experiment. I gave six investors the exact same AED 5,000,000, in the same market, over the same 30 years. The only thing that changed was how each one bought — mortgage or cash, full market price or distressed, short-term rental or long-term lease. Same starting capital. Same 10-year buying window. Same 2% annual inflation on both property values and rents. Then I let it run.

The gap between the best and worst outcome is not small. It's the difference between AED 11.7 million and AED 135.9 million from the identical AED 5 million start. Investor to investor, no agent spin — here's the full model, and here's the strategy I'd actually use with my own money.

Watch the full breakdown on YouTube, or keep reading for the numbers, the tables, and the risks I didn't have time to cover on camera.

The Methodology: One Rule, Six Paths

I built a 30-year model, verified to the dirham, with one fair-fight rule: every investor gets AED 5,000,000, fully deployed, nothing sitting idle. Whatever's left after the main units buys a cheaper studio (~AED 900,000) financed the same way, and any small remainder rolls straight into year-one reinvestment.

Every investor reinvests 100% of rental profit into buying more units for the first 10 years, then stops. From year 11 onward, the cash flow goes to their pocket instead of into new property. Property values and rents both grow at 2% a year — and critically, new purchases also cost the inflated price, so buying later genuinely gets more expensive. That's what keeps this realistic instead of a spreadsheet fantasy. Dubai's had a rougher and rosier decade than a flat 2%, but averaged out over 20+ years, 2% is a defensible number. There's zero income, property, or capital gains tax on any of it — Dubai keeps that part simple.

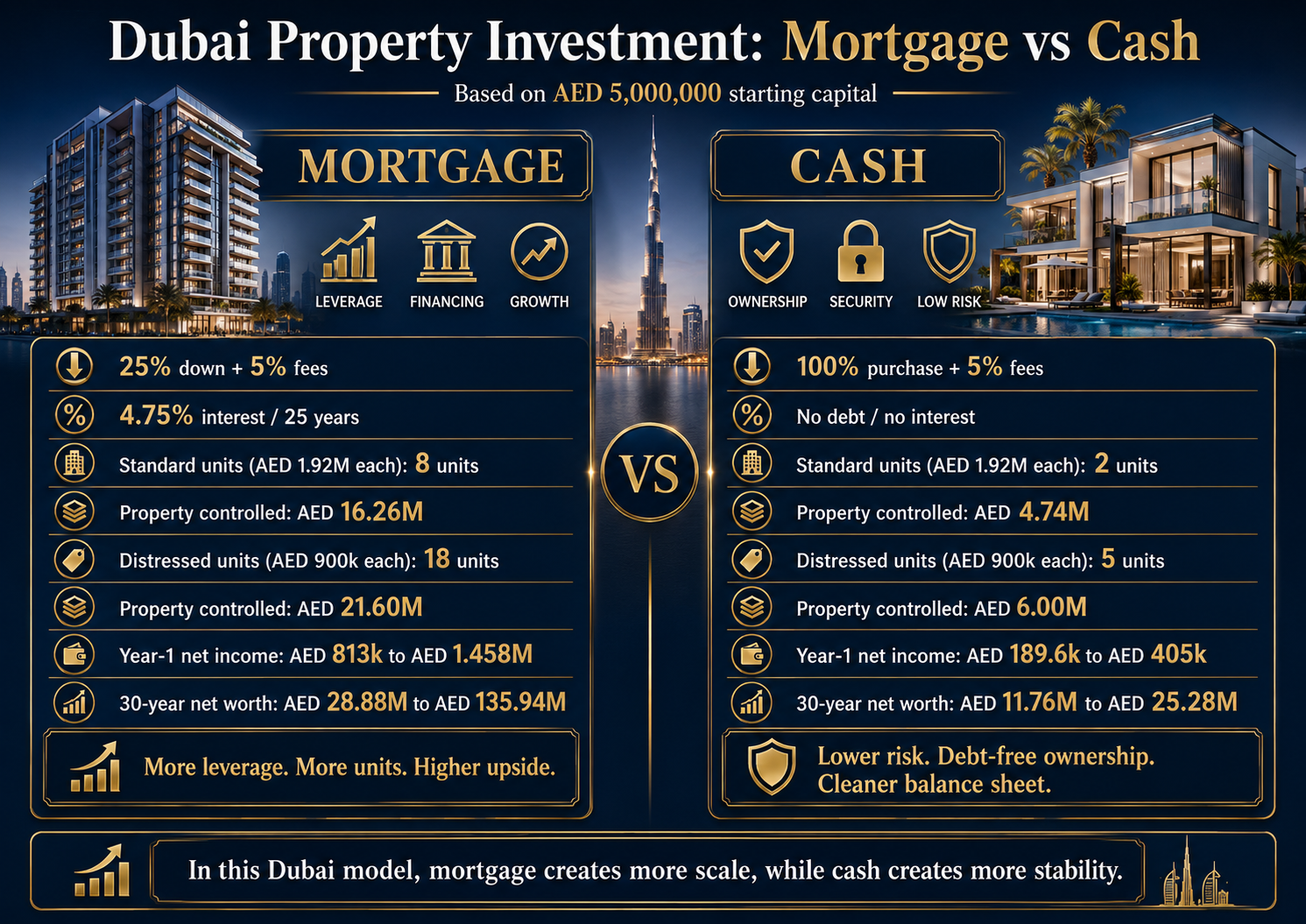

The two variables I tested: standard price (AED 1.92M) vs. distressed (AED 900k, worth AED 1.2M), and mortgage (25% down, 4.75% over 25 years, 5% fees) vs. cash. Short-term/mid-term rental mix on top for most of them, long-term for two, so you can see the yield gap in isolation too.

The Six Investors: What AED 5M Buys on Day One

Here's the setup — same AED 5,000,000 each, deployed six different ways:

InvestorStrategyPrice/unitUnits day 1Property controlled1Standard, Mortgage, Short-letAED 1,920,0008AED 16,260,0002Standard, Mortgage, Long-termAED 1,920,0008AED 16,260,0003Standard, Cash, Short-letAED 1,920,0002AED 4,740,0004Standard, Cash, Long-termAED 1,920,0002AED 4,740,0005Distressed, Mortgage, Short-letAED 900,00018AED 21,600,0006Distressed, Cash, Short-letAED 900,0005AED 6,000,000

Look at Investor 5 versus Investor 1 for a second. Same AED 5 million. Investor 1, buying at full market price with a mortgage, controls AED 16.26 million in property. Investor 5, buying the same type of unit below market with a mortgage, controls AED 21.6 million — and walks away with AED 5.4 million of instant equity on day one, because the true market value of what they bought (AED 1.2M) already exceeds the AED 900k they paid. That gap is the entire thesis of this model.

Year One: Who's Actually Making Money

This is the part most first-time mortgage buyers get wrong. Buy on mortgage at full market price, and you're underwater in year one — the net operating income doesn't cover the mortgage payment yet on a fresh purchase. Buy distressed, and you're in profit from day one, because you financed less than the unit is actually worth.

InvestorYear-1 net incomeReturn on the 5M1 — Std/Mortgage/STRAED 813,00016.3%2 — Std/Mortgage/LTAED 650,40013.0%3 — Std/Cash/STRAED 237,0004.7%4 — Std/Cash/LTAED 189,6003.8%5 — Dist/Mortgage/STRAED 1,458,00029.2%6 — Dist/Cash/STRAED 405,0008.1%

Investor 5's 29.2% year-one return on capital isn't a typo — it's what happens when leverage (mortgage) meets a genuine discount (distressed) meets the higher yield of short-term rental, all at once. That combination is doing three jobs simultaneously, and it shows immediately.

Ten Years In: The Buying Window Closes

Every investor reinvests for 10 years, then stops. This is where the gap between "buying often" and "buying right" actually opens up, because each reinvestment cycle compounds on whatever base you started with.

InvestorUnits ownedNet worth (equity)1 — Std/Mortgage/STR10AED 10,823,2472 — Std/Mortgage/LT9AED 10,123,3323 — Std/Cash/STR4AED 7,914,3254 — Std/Cash/LT4AED 7,914,3255 — Dist/Mortgage/STR68AED 57,813,6446 — Dist/Cash/STR12AED 17,012,494

By year 10, Investor 5 has scaled to 68 units and AED 57.8 million in equity — from the same AED 5 million everyone else started with. That's not a rounding difference from the other five; it's an entirely different outcome, driven by compounding a genuine discount with leverage over a decade of reinvestment.

Thirty Years Later: The Full Picture

This is the number that matters if you're buying property to actually retire on it, not just to watch the equity sit there.

InvestorNet worth (30 yrs)Income/month (pocket)Multiple on 5M1 — Std/Mortgage/STRAED 31,911,027AED 124,8926.4x2 — Std/Mortgage/LTAED 28,875,235AED 96,2515.8x3 — Std/Cash/STRAED 11,760,270AED 49,0012.4x4 — Std/Cash/LTAED 11,760,270AED 39,2012.4x5 — Dist/Mortgage/STRAED 135,941,501AED 638,22527.2x6 — Dist/Cash/STRAED 25,279,671AED 142,1985.1x

Notice Investor 3 and Investor 4 land on the exact same net worth — AED 11,760,270 — despite one running short-term and one running long-term rentals. That's not an error in the model; it's cash buyers with zero debt, so their net worth is just the property's appreciated value, which doesn't care what kind of lease is on it. What the rental strategy changes for a cash buyer isn't net worth, it's the monthly income you actually get to spend: AED 49,001 vs. AED 39,201 — a 25% difference, purely from professional short-term rental management capturing a better yield on the same asset.

And then there's Investor 5: AED 135.9 million, a 27.2x multiple on the identical AED 5 million everyone else started with. Investor 6, who bought the same distressed units but paid cash instead of financing them, still ends up at AED 25.3 million with zero debt and a clean balance sheet — which is its own kind of win if leverage keeps you up at night.

Why Distressed Still Wins, Even With 2% Inflation Working Against It

Here's the part that surprises people: new purchases also get more expensive under 2% inflation, so buying later should, in theory, slow you down. It does — but it doesn't erase the advantage of buying below market in the first place. Every distressed unit Investor 5 and Investor 6 buy, at every point in the 10-year window, still carries the same built-in discount to true market value. The compounding effect of leverage plus discount plus reinvestment outruns the drag of rising purchase prices, every single cycle. Buying right beats buying often — even when the "often" units cost more each year.

How Fast Investor 5 Actually Scales

The 30-year numbers get the headline, but the shape of the 10-year buying window is worth seeing on its own. Every year, Investor 5 reinvests all rental profit plus the studio-top-up remainder into more distressed units — and because the discount compounds on itself, the unit count doesn't grow in a straight line, it accelerates.

YearUnits ownedNet worth (equity)121AED 12,979,412327AED 18,520,016535AED 25,194,378746AED 36,079,7521068AED 57,813,644

Twenty-one units to sixty-eight in a decade, without adding a single dirham beyond the original AED 5,000,000. That's what buying right, compounded, actually looks like year by year instead of just start and finish.

The Real Cost of Distressed: What the Spreadsheet Doesn't Show

I'd be doing you a disservice if I made this sound easy, because it isn't. Distressed deals in Dubai — units in buildings that are 7-8+ years old, priced meaningfully below current market in areas like Dubai Marina, JLT, Downtown, Creek Harbour, or Business Bay — don't show up on a portal with a "distressed" filter. You find them by being in contact with a wide network of brokers, being patient through periods where sellers simply aren't motivated, and being ready to move fast when a genuine one appears. In the months around escalating regional tension, for example, deal flow slows to a crawl — that's exactly when patience matters most, not less.

Mortgage access is its own filter. Getting financed in Dubai without UAE-based income or an existing investment track record is genuinely difficult — banks want to see income and a relationship, not just a down payment. That's part of why I personally started with cash: it builds the track record that makes refinancing and future leverage possible later.

And short-term rental only outperforms long-term if it's run properly. Run it badly — wrong pricing, poor turnover, weak marketing — and you can end up making less than a simple annual lease, not more. The 20-30%, sometimes 40%, premium that short-let can generate over long-term only shows up with professional pricing, multi-channel distribution, and consistent guest turnover. That's an operating discipline, not a passive outcome. If you want the mechanics of what that actually looks like day to day, I broke it down in our Airbnb management deep-dive.

Who Should Run This Strategy

Investors with access to a genuine broker network and the patience to wait months for a real distressed deal, not a "discount" that's actually just list price with a friendly agent.

Investors who already have UAE income, an existing property, or a track record that makes mortgage approval realistic — leverage is where most of the outperformance in this model comes from.

Investors willing to hire (or become) a professional short-term rental operator, since the yield gap only shows up with real occupancy and pricing discipline, not a listing left on autopilot.

Anyone comfortable reinvesting profit for a full 10 years before taking any income home — this model is built for compounding, not immediate cash flow.

Who Should Think Twice

If you need income from year one, the mortgage-at-full-price paths (Investors 1 and 2) start underwater and stay tight for the first couple of years — plan your cash reserves accordingly.

If you don't have the broker relationships or patience for distressed sourcing, forcing it will likely mean overpaying for something you call "distressed" that isn't — at which point you've just bought a standard unit with extra steps.

If you can't stomach 25 years of mortgage exposure and want a clean, debt-free balance sheet, cash buying (Investors 3, 4, or 6) is the more comfortable path, even though it caps your multiple well below the leveraged distressed strategy.

If you're going to self-manage short-term rentals without the time or systems to do it properly, model your numbers on long-term yields instead — the short-let premium evaporates fast under bad management.

Key Terms, Explained (So the Tables Above Actually Make Sense)

Purchase price vs. true market value — what's the difference?

Purchase price is what you actually pay. True market value is what the unit is worth on the open market. For the four standard-price investors, those are the same number — you're paying full market rate. For the two distressed investors, there's a real gap: they pay AED 900,000 for a unit genuinely worth AED 1,200,000. That gap is the entire strategy.

What does "cash needed per unit" actually mean?

It's the money that actually leaves your account to close on one unit. Cash buyers pay the full price plus 5% fees. Mortgage buyers pay only the 25% deposit plus 5% fees — the bank covers the other 75%. That's why Investor 5 (mortgage, distressed) needed just AED 270,000 to control a unit, while Investor 4 (cash, standard) needed AED 2,016,000 for the same buying power.

What is "instant equity" on a distressed deal?

It only applies to distressed buyers — the gap between what you paid and what the unit is genuinely worth, banked the day you sign. Investor 5 walks away with AED 5,400,000 of instant equity on day one. Investor 1, buying at full market price, starts at zero; their equity only builds afterward, through mortgage paydown and appreciation.

Why does everyone end up buying a "studio top-up"?

It's how the fair-fight rule stays honest — every dirham working, nothing idle. Whatever's left after the main units buys a cheaper Marina studio (~AED 900,000), financed the same way as everything else. It's a small detail in the model, but it's the reason none of the six investors leave meaningful capital sitting in cash doing nothing.

The Bottom Line

Same AED 5,000,000. Same 10-year effort. Same realistic 2% inflation on values and on new purchases. Buying distressed still wins clearly — Investor 5 reaches both the largest portfolio and the largest income by combining leverage with a genuine discount, while Investor 6 owns the same discount strategy debt-free with strong, clean, tax-free monthly cash flow. Buying right beats buying often, even when later units cost more.

The smart play: if you can access financing and a real broker network, target distressed units below AED 1 million in established areas — Marina, JLT, Downtown, Business Bay — in buildings 7-8+ years old, finance them at 75% loan-to-value, and run them as professionally-managed short-term/mid-term rentals through the full 10-year buying window before switching to income mode. If leverage isn't available to you yet, the same distressed-unit strategy paid in cash still delivers a 5x multiple with zero debt — start there and refinance once you've built the track record.

Related reading if you want the two ideas either side of this one: why most Dubai investors underperform in the first place, and why I buy secondary and distressed instead of off-plan.

If you want to talk through which of these six paths actually fits your capital and your risk appetite — investor to investor, no sales pitch — WhatsApp me →